Source here.

Inflation seems to be waning. The conventional change from a year ago:

The month to month changes now suddenly more popular on the way down than it was on the way up:

I generally don't make predictions -- unconditional forecasting is a fraught game in economics. But I have been as far out on a limb this year as I ever have in thinking this is possible and even likely.

The standard fiscal theory 101 says that a $5 trillion fiscal blowout will lead to an increase in the price level, to inflate away outstanding debt. But that inflation eventually goes away, even if the Fed does nothing. It goes away a little faster if the Fed raises rates. The central graph: here's what happens in response to a big fiscal shock, if the Fed does nothing. Inflation rises but fades away as the new debt is inflated away.

So, while inflation was still increasing, starting here, last March, here at length for the Hoover monetary policy conference published as "inflation past present and future," more distilled here with the first draft of "fiscal histories," here with the clarity of continuous time models, here in the WSJ and here with pictures, here in the first draft of "expectations and the neutrality of interest rates," I did go out on a limb with the view that inflation would abate, even without the Fed dramatically raising interest rates. Then, updated here as inflation did after all start to ease. (Hmm, I seem to be making the same point a few too many times!)

I call this the "second great experiment," as conventional theory says the Fed needs to dramatically raise interest rates above current inflation to bring inflation down.

Now, to Luther's point. Is this not a victory lap for "team transitory," the view that inflation is just "supply shocks" that go away on their own?

No. A "supply shock" would raise prices temporarily, and then prices would fall back down to normal once the supply shock is over. A supply shock all on its own cannot permanently raise the price level. How is the price level doing?

The cumulative inflation has shifted up the price level by something like 10-20%, depending what you think about the earlier trend. The pure "supply shock" view says that we should now experience a symmetric period of deflation to bring the price level back to where it was, or at least to that plus a 2% trend. The fiscal theory or "demand" view says that this price level shock is permanent, or at least until something else comes along; a fiscal retrenchment would be necessary to lower the price level back to where it was.

Well, it hasn't happened yet. The current end of inflation does not prove the "supply shock" view right. Perhaps it will. If we get a period of 10% deflation, just as unrelated to Fed action as the inflation was, then the supply shock view can take a turn of "we told you so." Though, of course, nothing in economics is ever so simple.

What happens next? In the simple fiscal theory model, the Fed can lower inflation today, but only by making future inflation a bit worse. That is desirable too. For the recent Hoover economic policy roundtable, I made the following graph:

The beginning is the same as the last graph -- the response to a 1% fiscal shock when the Fed does nothing. Now I ask, what if the Fed waits a year and then starts raising rates. You see in the short run the Fed does bring down inflation faster than it would otherwise go down. However, we have to inflate away debt at some point unless fiscal policy wakes up and decides to pay it back more aggressively. So we get more inflation in the long run. I call that "unpleasant interest rate arithmetic."

This leads me to worry about a 1975ish future:

Inflation goes down without dramatic Fed intervention, we all cheer, but then it gets stuck maybe around 4%. And we wait for the next shock, amid eerily 1970s arguments that we should get used to inflation, raise the inflation target, it's too costly to bring it down, or that it's really all about worker-manager conflicts of price gouging anyway.

I'm more leery of this one however. The graph of the effects of monetary policy has more unsettled ingredients in it. Still, you have to go with the model you have, not the model you wish you had.

On a note of optimism, the long-run expected inflation and price level remain in the Fed's control, even in my fiscal theory model. After the fiscal blowout has been inflated away, the Fed can gently normalize. The stair step is not realistic of course, but designed to show the mechanism.

But some new fiscal or monetary shock will surely intervene before we see this. That's one of the main dangers of economic forecasting, what I called "unconditional" above. All we can hope to do is to say what is expected to happen, what will happen on average over many situations like our own. But what actually will happen depends primarily on whatever shocks hit us next. So as rhetorically attractive as it is to point fingers at the right field bleachers and announce where the home run will go, that's not how it works. Even if a prediction is the best it can be, right on average, it will be wrong about half the time. So beware evaluating any economic model, including mine, on single data points, and the rhetorical magic of ex ante predictions. On the other hand they do add up weight of evidence.

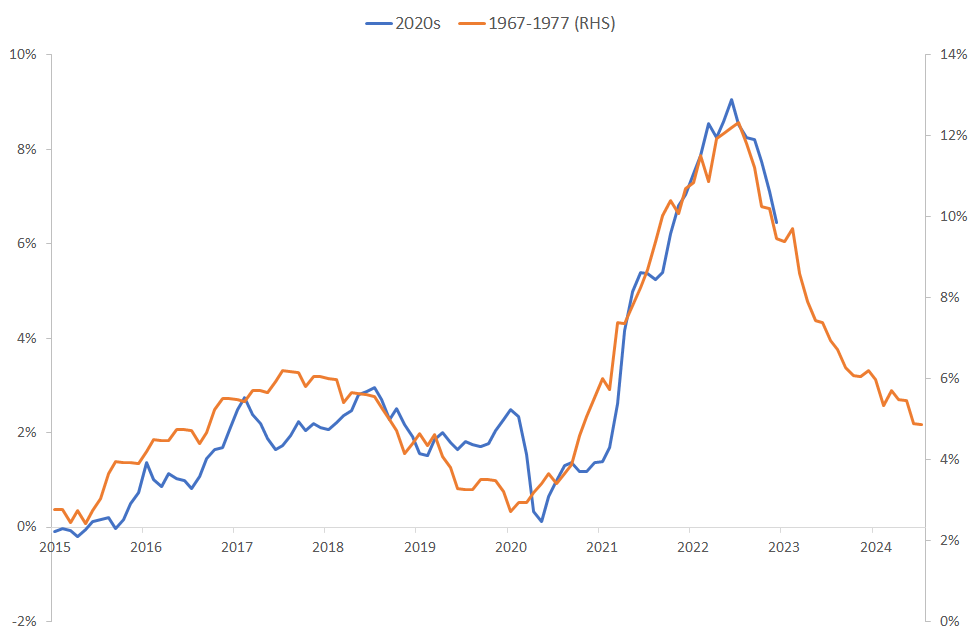

Update: Jesper Rangvid overlays inflation in the late 1960s through 1975 to inflation today,

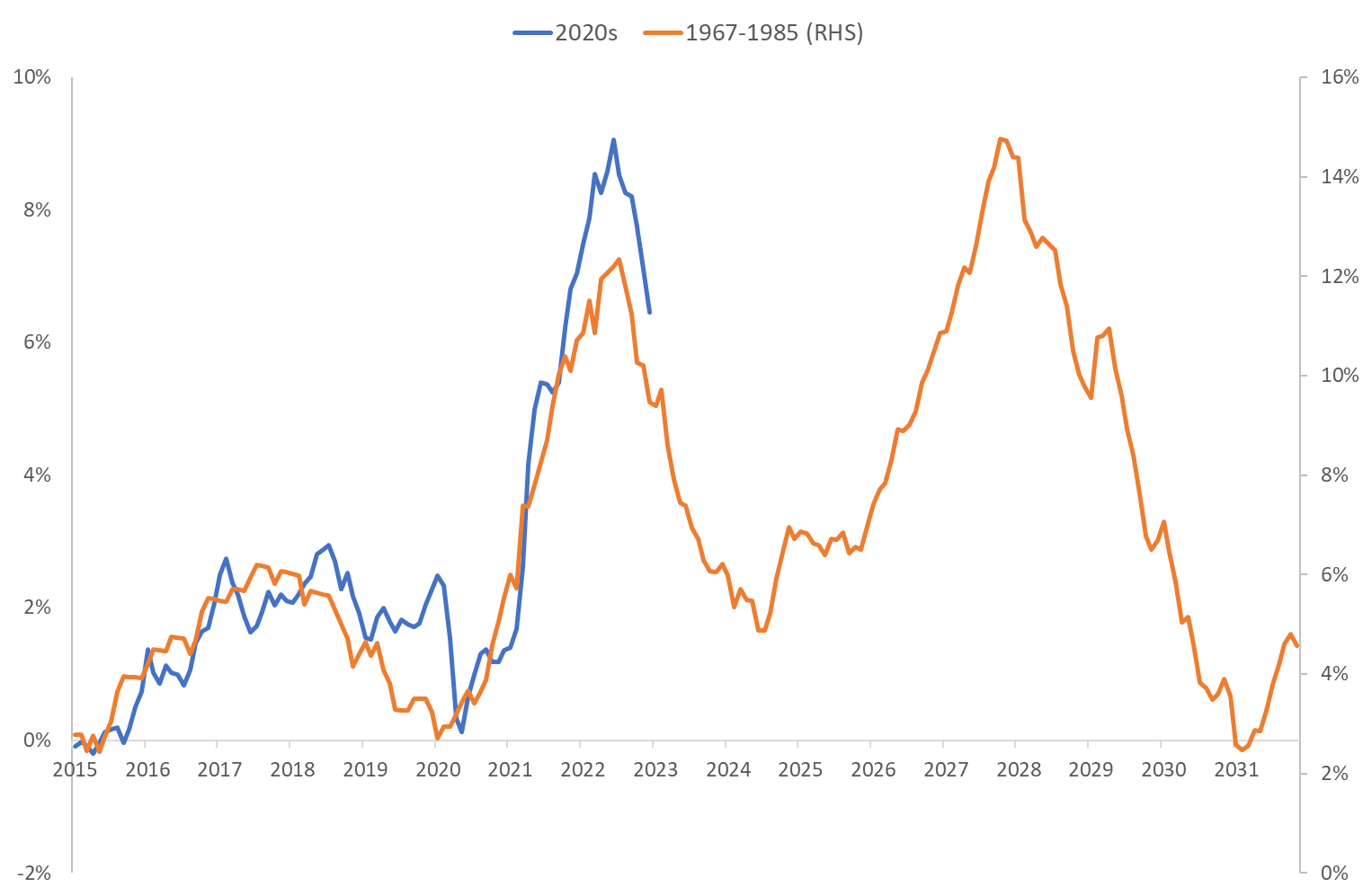

If this makes you feel better, he then plots inflation through the early 1980s,

Now you see more accurately my worry about our own future. Easing inflation, a recession, a fiscal blowout (1975 was the largest primary deficit since WWII), an oil shock, and here we go again.

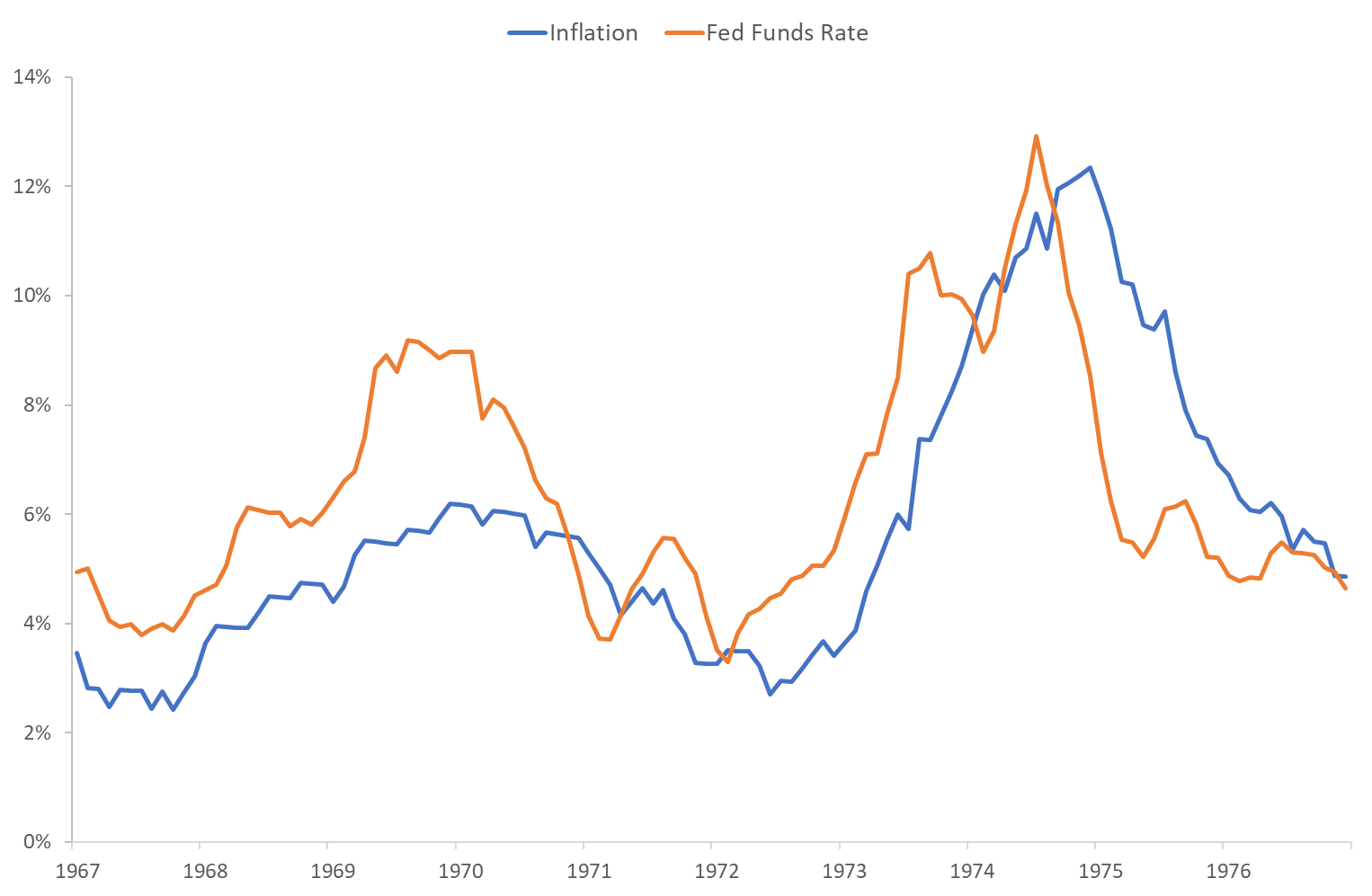

Jesper points out however the vastly different Fed response to inflation now vs. 1975. Then:

Now:

This comparison suggests one of two possibilities. 1) This time will be different. 2) The Fed is a lot less powerful for good or bad than you think.